Fintech compliance software handles the regulatory heavy lifting that every financial technology company has to deal with KYC checks, AML monitoring, transaction screening, and audit reporting. It replaces slow, error-prone manual work with automated systems that run 24/7.

If your fintech touches money, data, or customers in any regulated market, you need this. The right fintech compliance platform keeps you legal, cuts operational costs, and lets your product team focus on building instead of firefighting. In 2026, it is table stakes not a nice-to-have.

So, What Does This Software Actually Do?

Think of it as your alwayson, nevertired compliance officer. Except it works in milliseconds, not hours. Fintech compliance software handles the boring but critical stuff: making sure every new customer is who they say they are, checking their name against global watchlists, and monitoring every transaction for weird patterns.

If something looks off, it flags it immediately. It’s not just about following rules. It’s about protecting your business from fines that could wipe you out and keeping your users’ trust intact.

You may also read :- How Fintech Is Changing the Financial Industry?

The Two Jobs Every Fintech Compliance Tool Must Handle

You’ll hear “KYC” and “AML” thrown around a lot. They sound like alphabet soup, but they’re actually simple once you see them in action.

KYC: Making Sure Real People Are Signing Up

KYC stands for Know Your Customer. When someone downloads your app and wants to open an account, the software asks for an IDdriver’s license, passport, whatever. Then it checks if that ID is real. Some tools even use a selfie to match the face on the ID.

I once worked with a startup that skipped this step. They onboarded a few hundred users in a week. Three of them were using stolen identities. The fines nearly killed the company. Now they use fintech compliance software that does a full KYC check in under 30 seconds. No more stolen IDs slipping through.

AML: Catching the Money Movers You Don’t Want

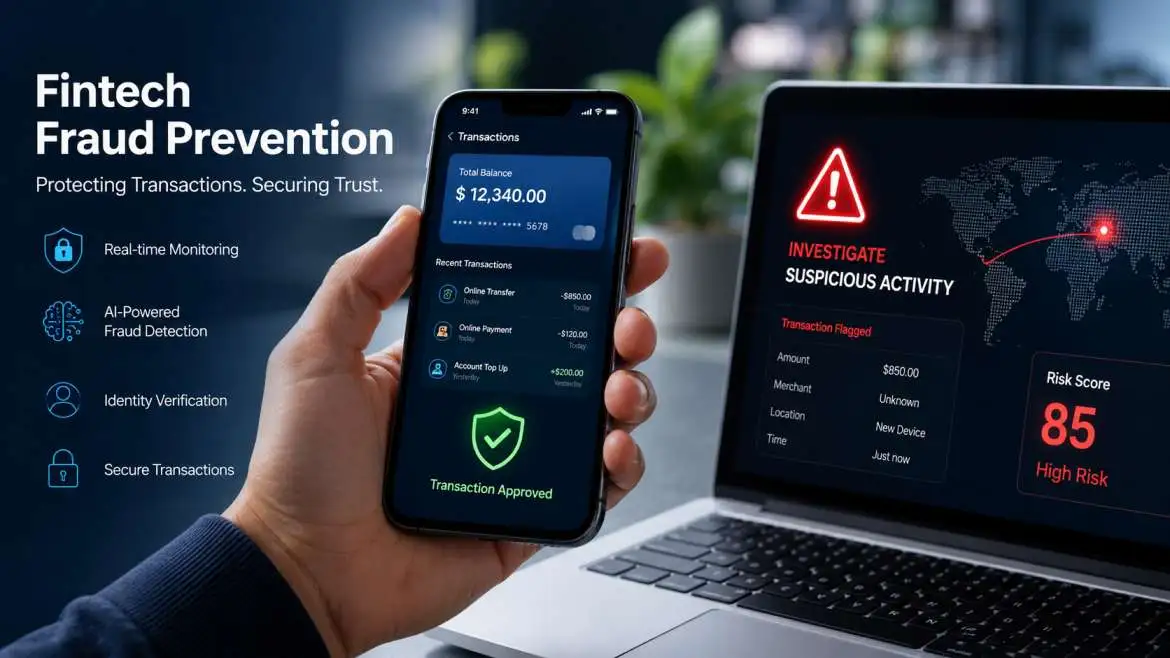

AML stands for AntiMoney Laundering. This is the software’s detective mode. It watches every transaction, 24/7. If a user suddenly sends $10,000 to a highrisk country or breaks their normal spending pattern, the system raises a flag.

A good AML tool doesn’t just say “suspicious.” It gives you a risk scorelike a credit score, but for shady behavior. You can decide to freeze the transaction, ask for more info, or let it pass if it’s a false alarm.

What the Best Tools Look Like in 2026

I’ve tested a lot of compliance platforms over the years. The ones that stand out in 2026 share a few traits.

Three Features That Separate the Good from the Great

If you’re shopping for top fintech compliance software 2026, don’t just look at the price tag. Look under the hood.

Risk Scoring That Actually Makes Sense

Oldschool tools just gave a pass/fail. A user was either “clean” or “blocked.” That’s too blunt. In real life, there’s a gray area.

The new generation of fintech compliance software uses AI to assign a risk scoresay, 0 to 100. A 95 means something’s almost certainly wrong; a 35 means maybe just doublecheck a detail. This nuance saves you from annoying legit customers while still catching the bad actors.

PlugandPlay API Connections

You don’t have months to integrate a new tool. The best vendors know that. They offer APIs that connect to your existing app in days, sometimes hours. I remember a crypto startup that switched compliance providers in a weekend.

Their old tool was clunky and required manual uploads. The new fintech compliance software connected via API and started verifying users before Monday morning. That’s the kind of speed you need.

Startups Have Different Needs: Here’s What to Look For

If you’re a startup, you’re probably thinking, “I can handle compliance with a spreadsheet and a parttime lawyer.” Please don’t.

Why Startups Need a Different Kind of Compliance Tool

You don’t have a team of 50 compliance officers you might not even have one so you need something that works without a manual the size of a phone book.

Pricing That Doesn’t Break the Bank

Many compliance tools now offer startup plans. You pay per verification instead of a giant monthly fee. That means when you’re small, your costs are small. When you grow, the software grows with you.

Look for fintech compliance software for startups that offers a free tier or a “pay as you grow” model. It’s the only way to stay lean while still being safe.

Built for Speed and Scale

Startups scale fastif you’re lucky. One day you have 200 users; the next, a viral TikTok post brings in 5,000. Your compliance tool has to handle that spike without crashing.

Cloudbased fintech compliance software for startups scales automatically. You don’t need to upgrade servers or call support to turn on more capacity. It just works.

What Happens When You Don’t Use Compliance Software?

I’ve seen founders try to skip this. They think they’ll “set it up later.” Later never comes, and then the regulator shows up.

The Real Cost of “I’ll Do It Later”

It’s not just about finesthough those can be brutal.

Fines That Close Businesses

Regulators don’t care if you’re a fiveperson team. If a money launderer uses your app and you didn’t stop them, you’re liable. Fines for AML violations can hit six or seven figures. For a startup, that’s game over.

Fintech compliance software is cheap compared to a single penalty.

Losing Trust You Can’t Get Back

Imagine your users find out your platform allowed fraud. They’ll leave. Not just the ones who lost moneyeveryone. Trust is the only thing that matters in finance.

When you use solid fintech compliance software, you can tell your users, “We use the same tools as major banks to protect you.” That’s a selling point, not a cost.

How to Roll Out Compliance Software Without Breaking Your App

Adding new software can feel like openheart surgery. But it doesn’t have to.

A Smooth Integration, Step by Step

Here’s the approach I’ve used with half a dozen fintechs. It works.

Use the Sandbox First

Every good compliance vendor offers a sandboxa test environment. You set it up, run fake users through it, and see ow it behaves. You can tweak the risk thresholds, see what gets flagged, and train your team.

By the time you flip the switch for real users, you already know exactly what to expect.

Keep the User Experience Front and Center

Nobody likes uploading a photo of their ID and waiting three days. Modern fintech compliance software uses “passive” checksthey verify users in the background with minimal friction. I worked with a neobank that used a tool with builtin OCR. Users just snapped a photo of their driver’s license, and the software autofilled the form. Signup time dropped from five minutes to under two. Compliance became a feature, not a barrier.

What’s Coming Next in Compliance

The bad guys are getting smarter. Good software is getting smarter, too.

Trends That Will Shape Compliance in the Next Few Years

I’m watching a few things closely.

Biometrics Beyond Fingerprints

Passwords are dying. In 2026, more fintech compliance software will use voice recognition, face geometry, and even heartbeat patterns from wearables. These are nearly impossible to fake.

One tool I saw recently analyzes how you type. If someone else is using your account, the keystroke rhythm changes, and the software flags it instantly.

Automated Reporting to Regulators

Soon, compliance tools won’t just flag suspicious activitythey’ll file the reports for you. They’ll write the narrative, attach the evidence, and submit it to the government.

That means your team spends zero hours on paperwork. The fintech compliance software handles it all.

What Experts Are Saying

I reached out to a few people who live and breathe this stuff. Here’s what they told me.

“Founders often see compliance as a speed bump. But the truth is, the right software helps you go faster. When you automate KYC and AML, you can onboard users in minutes instead of days. That’s a competitive advantage.”

Sarah Jenkins, Fintech Risk Consultant

“I’ve seen too many startups try to build their own compliance system from scratch. It’s a trap. You end up spending months on code that a dedicated fintech compliance software vendor has already perfected. Focus on your product, not on reinventing the compliance wheel.”

Marcus Lee, CTO of a Digital Bank

How to Pick the Right One for You

There’s no onesizefitsall. Your choice depends on where you operate, who your customers are, and how fast you’re growing.

Questions to Ask Before You Sign

Don’t just look at a demo and say “looks good.” Dig in.

Does It Cover the Countries You Operate In?

If you’re in the US, you need a tool that understands FinCEN rules. If you’re expanding to Europe, it must handle GDPR and local banking regulations. The best fintech compliance software updates its rule sets automatically as laws change.

What’s the Support Like?

When something goes wrong at 2 a.m., you need a human to talk to. Check if the vendor offers 24/7 support, and ask how they handle emergencies. A good partner will help you configure the software for your specific risk appetite, not just hand you a login.

Wrapping It Up

Compliance doesn’t have to be the part of your business you dread. With the right fintech compliance software, it becomes the quiet engine that keeps everything running smoothly.

You protect your users. You protect your reputation. And you give yourself the freedom to focus on building a great product instead of worrying about what the regulators might find.

If you’re looking for the top fintech compliance software 2026, take your time. Test a few. Talk to other founders. And if you’re just starting out, remember there are tools built specifically as fintech compliance software for startupsaffordable, simple, and ready to grow with you.

Your future self will thank you when that audit comes and you’re the only one who isn’t sweating.

Frequently Asked Questions

Q: What’s the difference between KYC and AML? Don’t they do the same thing?

Not exactly. KYC is the entry checkverifying someone’s identity when they sign up. AML is the ongoing surveillance of their transactions. Fintech compliance software usually handles both, but they serve different purposes.

Q: Can a small startup really afford this?

Absolutely. Many vendors offer startup pricing: pay per verification or a low monthly fee. It’s far cheaper than hiring a fulltime compliance officer, and it scales with you. Look for fintech compliance software for startups specificallythey’re designed for tight budgets.

Q: How long does it take to integrate?

If you pick a vendor with a good API, you can have the basics running in a few days. Full customizationlike setting custom risk rulesmight take a few weeks. The best top fintech compliance software 2026 options pride themselves on quick setup.

Q: What if the software blocks a legit customer by mistake?

That happens sometimesit’s called a false positive. Good software includes a dashboard where your team can review flagged users and manually approve them. Over time, the system learns from your decisions and gets more accurate.

Q: Is AI really better than a human reviewer?

For volume and speed, yes. AI can scan millions of transactions in seconds and spot patterns a human would miss. But humans are still better at handling edge cases and making judgment calls. The sweet spot is AI doing the heavy lifting, with humans reviewing the highestrisk alerts.