Money is moving faster than ever. You can send cash to a friend in seconds. You can buy things online with one click. You can take a loan on your phone. This is called fintech. It means financial technology. It is great for people. But bad guys also love fintech. They use it to steal money. They find small gaps in the system. They trick people. They make fake accounts. They take money that is not theirs.

This is a big problem. Every year, people and companies lose billions of dollars. Banks lose money. Small businesses lose money. Normal people like you and me lose money. That is why we need fintech fraud prevention.

Fintech fraud prevention is a set of rules and tools. These rules help stop bad guys before they take money. These tools check every payment. They look at every new account. They see if someone is lying. They work very fast. You do not even see them working.

In this article, we will learn how fintech fraud prevention works. We will look at the best tools. We will name the top companies that keep your money safe. We will also see how new technology helps stop fraud. This is a full guide. No hard words. No tricky terms. Just straight talk.

What Is Fintech Fraud? Why Should You Care?

First, let us understand the problem. Fintech fraud is when a bad person uses digital money tools to steal. This is not like old bank fraud. Old fraud needed fake checks or a mask in a bank. New fraud happens on a phone or a laptop. It is fast. It can cross many countries. One bad guy in another country can steal from a thousand people in one night.

Here are some real examples.

A bad guy makes a fake website. It looks like your bank. You type your password. Now he has it. He takes your money. A bad guy buys stolen credit card numbers on the dark web. He uses them to buy gift cards. You do not know until you see your bill.

A bad guy creates a fake loan app. You need money. You download it. You give your ID and bank info. Then nothing happens. But he now has everything to empty your real account. A bad guy sends you a text. It says your bank account is frozen. Click this link to fix it. You click. You lose everything.

These things happen every day. They happen to smart people, too. They happen to old people. They happen to young people. Bad guys are clever. They know how to push your buttons. That is why companies need fintech fraud prevention. They cannot just hope bad guys stop. They need tools that fight back.

You may also read :- Top Fintech Compliance Software in 2026: Best Tools for KYC, AML and Risk Control

How Does Fintech Fraud Prevention Work? (Easy Explanation)

Think of a big fence around your money. That fence has many gates. Each gate has a guard. The guard asks questions. Who are you? Where is this money going? Does this look normal? If something looks wrong, the guard stops it.

Fintech fraud prevention is that fence. It works in three simple steps.

Step One: Check the Person

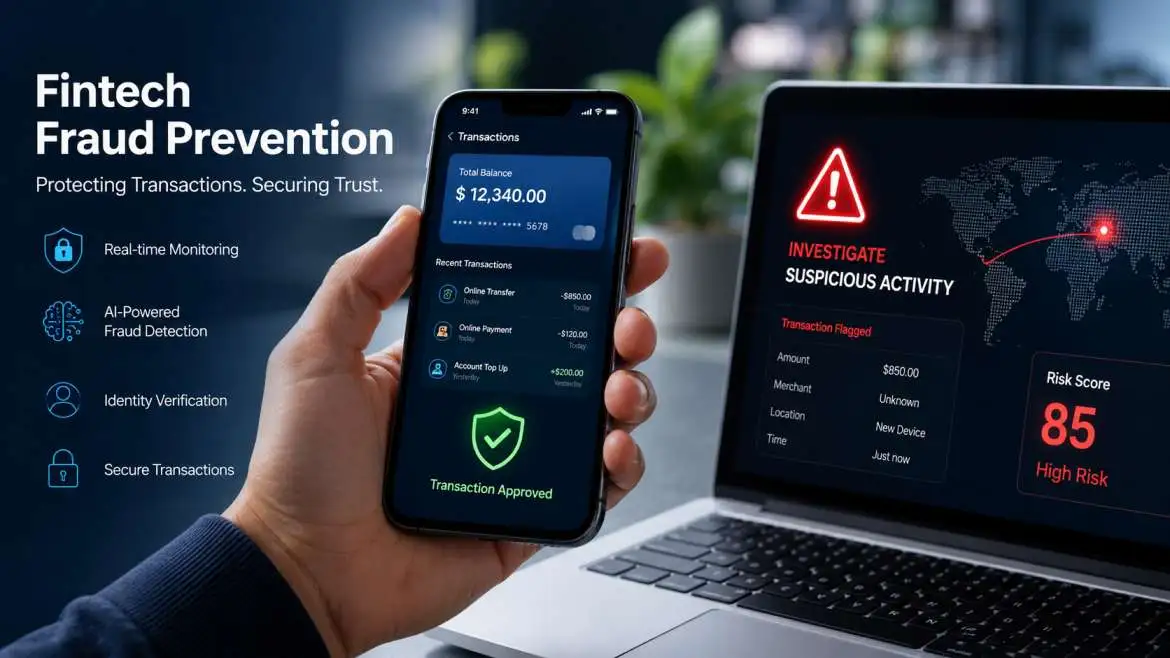

Every time you log in or pay, the system checks you. It looks at your device. It looks at where you are. It looks at how you type. If you always log in from New York, but today you log in from Russia, the system gets worried. It might ask for a code from your phone. That is fraud prevention working.

Step Two: Check the Action

Let us say you buy a coffee for five dollars. That is normal. But if you suddenly try to send ten thousand dollars to a country you never used, that is not normal. The system stops it. It might call you or text you. It asks, "Did you do this?" If you say yes, it lets it go. If you say no, it blocks it.

Step Three: Look for Patterns

Bad guys do not just steal once. They steal many times. They use the same tricks. Fintech fraud prevention tools learn these tricks. They see that many bad guys do the same thing. They then block that trick for everyone. This happens in real time. It takes less than a second.

Fintech Fraud Prevention Software: The Engine That Keeps Money Safe

We cannot stop fraud with just rules. We need software. Fintech fraud prevention software is a program. It runs in the background. It watches every transaction. It never sleeps. It works on holidays. It works at 3 AM. That is when bad guys try to strike.

One: It Learns You

The software watches how you use money. It learns your habits. It knows you buy gas on Friday. It knows you pay rent on the first of the month. It knows you never buy things at 2 AM. When something breaks this pattern, the software pays attention.

Two: It Looks at Devices

Every phone and computer has a fingerprint. Not your real finger. A digital fingerprint. It is a set of hidden numbers. Bad guys try to hide. They use fake names. But they cannot change their device fingerprint easily. The software sees this. It says, "Hey, this phone was used for fraud yesterday." So it blocks it today.

Three: It Checks the Network

Bad guys often work together. They use the same internet cafes or same VPNs. The software keeps a list of bad internet addresses. If a transaction comes from a bad address, the software blocks it. No questions asked.

Four: It Sends Alerts

When the software finds something strange, it tells someone. It sends a message to the fraud team at the company. That person then looks at the case. They decide to block or allow. The best software also sends you a text. Did you just try to buy a TV in another country? If not, call us now.

This software is not one size fits all. A small online store needs different software than a big bank. But all good software does these four things.

The Best Fintech Fraud Prevention Tools You Should Know

There are many tools out there. Some are free. Most cost money. The best ones save you more money than you pay. Here are the top tools that companies use right now. These are not hard to use. They are made for real people.

Tool One: Device Fingerprinting Tools

These tools look at the visitor's device. They give each device a unique ID. If a bad guy tries a hundred times with different names, the tool sees the same device. It blocks every try. Some good names in this space are FingerprintJS and ThreatMetrix. They are used by big apps and small shops.

Tool Two: Real-Time Transaction Monitoring

This tool looks at each payment as it happens. It checks the amount, the time, the location, and the past behavior. If the risk is high, it blocks. If the risk is medium, it asks for more proof. If the risk is low, it lets it pass. Companies like Forter and Riskified are leaders here. They process billions of dollars. They catch bad guys before they take a cent.

Tool Three: Identity Verification Tools

Before you open an account, the tool checks your ID. You take a picture of your driver license. You take a selfie. The tool compares them. It also checks if the ID is fake. These tools are very good now. They can spot a fake ID in seconds. Onfido and Jumio are two big names. They help banks and crypto apps.

Tool Four: AI-Powered Fraud Detection

This is the new smart tool. It uses a type of computer that learns. It does not follow fixed rules. It looks at millions of transactions. It finds new tricks that bad guys just invented. Then it blocks them. This tool gets better every day. Companies like Sift and DataVisor use this. They stop fraud that other tools miss.

Tool Five: Chargeback Protection Tools

A chargeback is when you tell your bank a transaction was fraudulent. The bank takes money back from the seller. That hurts the seller. Good tools stop fraud before it becomes a chargeback. They also help sellers win disputes. Kount is a good example. Now part of a bigger company. But still strong.

These tools are not secrets. Any fintech company can buy them. The best companies use more than one. They stack them like walls.

Top Fintech Fraud Prevention Companies That Lead the Market

Some companies are famous for stopping fraud. They build the best tools. They work with big banks and small startups. Let us look at who they are.

Company One: Sift

Sift started many years ago. They were one of the first to use smart computers for fraud. They help apps like Uber and Airbnb. They look at user behavior, device data, and past fraud patterns. They assign a risk score for every action. A high score means a block. A low score means "allow." Very simple. Very effective.

Company Two: Forter

Forter promises to catch fraud in real time. They process over 250 billion dollars in orders every year. They use a big network of stores. When one store sees a bad guy, all stores learn. That is powerful. Forter also offers chargeback protection. If they say a sale is safe, but it turns out to be fraud, they pay the loss. That is a big promise.

Company Three: Riskified

Riskified works mostly with online stores. They help stores sell more by blocking fewer good customers. Many fraud tools block too many real people. That loses money. Riskified is better at telling good from bad. They also guarantee their work. If they say a sale is safe and it is fraud, they cover the loss.

Company Four: SEON

SEON is newer. They focus on fast and easy setup. You can start using them in a day. They look at social media, email, phone number, and device. They give a simple yes or no. Many small fintech companies love SEON because it is cheap and easy.

Company Five: DataVisor

DataVisor is for big companies. They look at groups of bad actors. They do not just look at one transaction. They look at how bad guys work together. They find fraud rings. That is when many people work together to steal. This is hard to catch. DataVisor does it well.

Fintech Fraud Prevention Solutions: Not Just Software, But a Plan

Software is not enough. You need a full plan. A good plan has three parts. Software is one part. The other two parts are people and rules.

People Part

You need a team. Even one person can help. This person watches the alerts. They check suspicious cases. They answer customer calls. They learn from past fraud. A good fraud person is curious. They ask why. They look for small signs. They stop big losses.

Rules Part

You need clear rules. What amount triggers a check? What countries are high risk? How many times can someone try a password? These rules must be written down. Everyone must follow them. Review the rules every month. Bad guys change. So must your rules.

Software Part

Pick the right tool for your size. A small app with a few thousand users does not need a huge expensive tool. Start small. Use a simple tool. As you grow, add more. Do not buy everything at once.

A full solution is not one thing. It is many things working together. That is how you win.

The Role of AI in Fintech Fraud Prevention (Simple Words)

You hear the word "AI" a lot. It stands for artificial intelligence. In simple words, AI is a computer that learns. You do not tell it every rule. You show it many examples. It figures out the rules by itself.

AI is very good for fraud prevention. Here is why.

Old fraud tools used fixed rules. If the amount is more than 1000 dollars and the country is Nigeria, then block. That works for a while. Then bad guys learn. They sent 999 dollars from a different country. The old tool misses it. AI tools do not have fixed rules. They analyze everything — the transaction amount, the timing, and the device being used.The email address. The typing speed. The mouse movement. They put all this together. They find fraud that has no single obvious sign.

For example, AI can see that fraudsters often type slower on the password field. Real users type fast. Fraudsters copy and paste. AI sees this tiny difference. It then blocks them. A human would never notice this. AI also gets better over time. It learned a new trick today. It learns it tonight. It blocks it tomorrow. That is fast. That is powerful.

But AI is not perfect. Sometimes it blocks a real person. That is called a false positive. Sometimes it lets a bad guy through. That is a false negative. Good companies work hard to lower both. They use AI plus human reviews. That is the best way.

Real Life Example: How One App Stopped Fraud

Let me tell you a true story. A small money transfer app had a problem. Bad guys were making fake accounts. They would sign up with stolen IDs. They would send small amounts to each other. Then they would cash out. The app lost 50,000 dollars in one month.

The app owner was worried. He did not have a big team. He did not have a big budget. He bought a simple fintech fraud-prevention software. It had device fingerprinting and AI.

In the first week, the software found 200 fake accounts. They all came from the same three devices. The bad guys had reused their phones. The software blocked all those devices. No new fake accounts from those phones.

In the second week, the AI found a new pattern. Bad guys were signing up at 4 AM. Real users signed up during the day. The AI set a rule. Block all accounts made between 3 AM and 5 AM from new countries. That stopped another 100 fake accounts.

In one month, the app cut fraud by 90 percent. They paid 200 dollars a month for the software. They saved 45,000 dollars. That is a good deal.

Common Mistakes Companies Make

Many companies try to stop fraud. But they make mistakes. Here are the big ones.

Mistake One: Being Too Strict

Some companies block everything that looks even a little strange. That stops fraud. But it also stops real customers. Real customers get angry. They leave. You lose more money from lost sales than from fraud. Good fraud prevention is a balance. Block the bad. Let the good times pass.

Mistake Two: Being Too Lazy

Some companies do nothing. They hope fraud does not happen. That is stupid. Fraud will happen. It will hurt you. It will hurt your customers. Do not wait. Start with a simple tool today.

Mistake Three: Not Updating

Fraud changes every week. What worked last month may not work today. Update your rules. Update your software. Read fraud news. Talk to other companies. Stay awake.

Mistake Four: Ignoring Small Fraud

Some companies only care about big losses. They ignore small five-dollar frauds. That is a mistake. Bad guys start small. They test your system. If you ignore small fraud, they come back with big fraud. Stop every fraud. No matter the size.

The Future of Fintech Fraud Prevention

What comes next? Fraud will get smarter. But prevention will also get smarter. We will see more AI that watches video. Bad guys use deepfakes. That is a fake video of your face. Future software will spot these fakes. It will look at tiny eye movements. It will look at skin texture. It will know real from fake.

We will see more cooperation. Banks will share fraud data with each other. One bank sees a bad guy. All banks block him. That is coming soon. We will see faster payments with better checks. Real-time payments are great. But they leave no time to think. Future tools will check everything in milliseconds. They will make a decision before you blink.

We will see more tools for normal people. Not just for companies. Apps that warn you before you click a bad link. Apps that freeze your card with one tap. Apps that scan the dark web for your email. These exist now. They will get better. The future is not scary. It is just new. And new tools will keep us safe.

Final Words

Money is too hard to earn. You should not lose it to some bad guy sitting in a dark room. Fintech fraud prevention is not a fancy extra. It is a must-have. It protects your hard work. It protects your customers. It protects your sleep. The tools are here. The companies are ready. The software is cheap. There is no excuse. Start small. Start today. Do not wait for fraud to find you. Find it first. Block it. Move on.

Your money is yours. Keep it that way.