The global financial technology sector is changing fast due to sharp updates in government oversight. To help your business survive, this complete guide provides the latest fintech regulations news directly from the frontline. The modern financial space demands active compliance strategies, strict data privacy protocols, and deep security audits to protect consumer data and prevent major financial crime. By learning these rules, you will secure your digital tools, protect your regular users, and discover fresh paths for growth in today's digital market.

Why Regulatory Compliance Matters for Modern Startups?

Staying ahead of the rules is no longer just a task for your legal team. It is a core business need. Government watchdogs do not want to see plain paper policies anymore. They want to see those rules working in real-time. If you run a platform, you must show operational maturity to keep your partner banks happy and retain your customer trust.

Failing to follow these standards brings heavy costs. Watchdogs are handing out large fines, halting business launches, and shutting down weak platforms. To build a strong business that lasts, you must weave security and rules directly into your core engineering pipeline.

You may also read :- How Fintech Innovations Changed My Financial Life

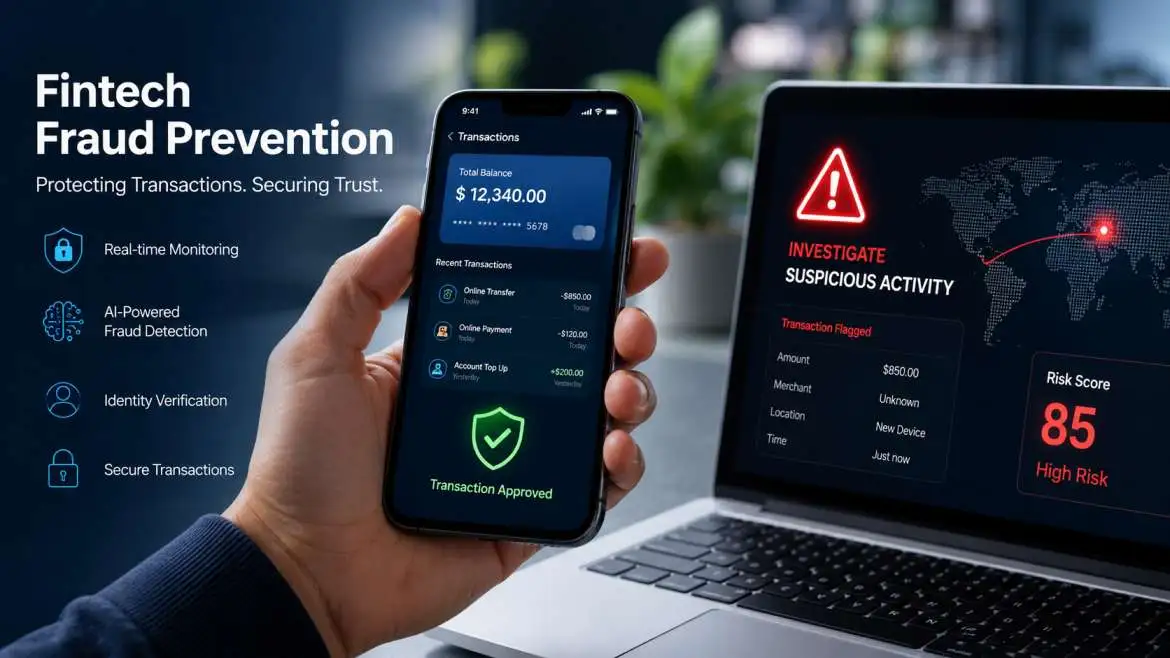

Direct Update: The Latest Fintech Regulations News

When we look at the core fintech regulations news, the biggest shift centers on how agencies view tech platforms. Watchdogs are treating digital applications just like traditional banks. This means your consumer lending tools, mobile wallets, and financial systems must face the same deep audits as local banks.

Regulatory groups like the Consumer Financial Protection Bureau are rewriting the book on consumer data portability. In the past, companies could quietly collect and use user details. Today, you must provide clear opt-out systems, use plain language in your user agreements, and build safe pathways to share information without leaks.

Understanding Financial Crime Prevention and Open Banking

To protect the financial landscape, world governments are updating their anti-money laundering frameworks. This directly changes how platforms handle user onboarding. You must verify every single identity through strict background checks.

"Compliance is not a checklist item; it is the foundation of digital trust. Companies that build transparent pipelines win the market." — Senior Regulatory Analyst

At the same time, open banking frameworks require companies to share financial details safely. If your system connects to external accounts, you must deploy uniform programming interfaces. These tools let users move their personal financial history between services freely without exposing their private passcodes to bad actors.

The Rising Impact of Artificial Intelligence in Audits

Artificial intelligence now drives many basic internal workflows. Companies use these automated systems to catch fake accounts and review loan applications. Because these models make major choices, watchdogs are demanding total transparency.

You must document every piece of data your automated models use. If a machine turns down a user for a line of credit, you must explain the exact reason behind that choice. Watchdogs want to make sure your algorithms do not discriminate against specific groups of people.

Major Policy Shifts Impacting Cross-Border Money Movement

Moving capital across borders used to take days and cost high hidden fees. New laws are forcing the industry to update its legacy systems. This change is making international transfers run much faster while forcing platforms to stay highly secure.

These international updates aim to connect different country systems together smoothly. If your platform moves money between continents, you must track these global shifts. You have to align your operations with both local rules and foreign laws to avoid blocked transfers.

European Changes and Instant Payment Rules

Europe is leading the charge with its updated Payment Services frameworks and the Digital Operational Resilience Act. These rules push companies to offer instant transfers to every citizen at no extra cost. The goal is to make digital retail transactions happen in seconds.

These rules also force companies to build stronger walls against internet fraud. If a user loses money due to a weak link in your software, your business may have to pay for those losses. This means your development team must test every update before launching it live.

Consumer Protection and Lending Standards

Watchdogs are clamping down on short-term consumer credit tools, such as popular buy-now-pay-later services. New consumer credit updates require deep checks on a person's ability to pay back their debts. This prevents shoppers from taking on more debt than they can handle.

Lenders must present all fees clearly before a user signs an agreement. You cannot hide charges in long terms-of-service pages. If your software uses tricky designs to push users into debt, you will face swift penalties from consumer protection agencies.

The Growth of Regulated Digital Assets and Stablecoins

Digital tokens and stablecoins are moving out of the wild west phase. Major countries are passing laws that give these tools a clear legal status. This means enterprise companies can finally use them for regular treasury tasks and vendor payments.

These laws help eliminate the wild price swings that used to ruin digital assets. When stablecoins have solid backing, businesses can use them to settle balances instantly. This reduces the risk of currency values changing while a transfer is in mid-flight.

Blockchain Tracking and Sanctions Compliance

Because digital ledger transactions are permanent, watchdogs use advanced tracking tools to watch public networks. Your business must screen every incoming wallet address against global sanction lists. You cannot accept tokens that have touched darknet marketplaces or illegal mixers.

Building these filtering systems requires robust software integration. Your platform must automatically block suspicious wallets before they can interact with your pool of funds. This keeps your business safe from international legal action.

Building a Bulletproof Infrastructure for Your Platform

To survive this era of heavy oversight, you need to change how you build software. Security cannot be a secondary thought that you patch on right before a launch. It must be the foundation of your entire engineering setup.

You should store all user data using high-grade encryption methods. Your teams must run regular simulations to see how your database holds up against simulated cyber attacks. If a breach occurs, you need automated systems that instantly isolate the damaged sectors to stop data leaks.

Vendor Management and Third-Party Risk

Most startups rely on third-party software vendors for tasks like cloud storage and identity checks. Under modern rules, you are fully responsible for the security flaws of your partners. If your identity vendor suffers a breach, the watchdogs will hold your platform accountable.

You must run deep due diligence checks on every vendor before signing a contract. Demand clear proof of their security practices and run your own tests on their connection points. Keep your vendor network clean and small to reduce your overall surface risk.

Essential Steps to Protect Your Financial Operations

To help your team stay fully compliant without slowing down your product development, follow this clear roadmap.

1. Assign Clear Compliance Ownership: Week 1.

Appoint a dedicated compliance officer to lead your regulatory strategy. This person will track policy updates, manage partner bank relationships, and oversee internal audits.

2. Draft Practical Operational Procedures: Weeks 2-3.

Write explicit instructions that map out exactly how your team handles consumer data, flags weird transactions, and escalates security events. Avoid vague checklists.

3. Deploy Real-Time Monitoring Systems: Weeks 4-5.

Install automated software tools that scan your platform for fraud and track data access. Set up immediate alerts for any system anomalies or unauthorized access attempts.

4. Run Full Team Simulation Drills: Week 6.

Test your team's readiness by staging a fake data breach or a sudden regulatory audit. Use the results to fix weak spots in your communication and system recovery plans.

Frequently Asked Questions

What is the main focus of recent fintech regulations news?

The latest updates focus heavily on operational reality. Watchdogs want to see that your security policies match your daily engineering actions. They are looking closely at how companies protect user data, audit automated models, and monitor third-party vendors.

How do new rules affect partnerships between banks and tech platforms?

Traditional banks now face massive pressure to supervise their digital partners closely. This means your platform will undergo much deeper due diligence checks during onboarding. You must provide clear documentation of your internal security controls to maintain these relationships.

Do small startups have to follow these strict compliance laws?

Yes, asset size does not exempt a platform from consumer protection laws. If your software handles consumer funds or processes personal financial data, you must follow local privacy laws and financial crime rules from day one.

What are watchdogs looking for when reviewing financial models?

Regulators want to see total transparency in algorithmic decision-making. You must prove that your credit models do not use biased metrics. Your team must be able to explain the exact data points that led to any automated user rejection.